Why Banking Needs a Platform-Powered AI Transformation

From fragmented systems to intelligent enterprises, why banks must rebuild their digital core to stay competitive

The banking sector is entering one of the most defining phases in its technological evolution. Over the past decade, digital transformation brought speed and accessibility, but the next wave is about intelligence, enabling systems to predict, reason, and act with context. As financial institutions navigate tighter margins, evolving regulations, and the growing expectations of a digital-native customer base, the focus has shifted from digitization to cognition. Banks today are expected not only to deliver faster experiences but also to anticipate risk, personalize engagement, and make every operational decision data-driven. (BCG)

A modern AI-powered transformation cannot happen without the right foundation. Most banks still operate on fragmented architectures where customer data, transactions, and risk models exist in isolated silos. These disconnected systems make AI adoption difficult, leading to inconsistent insights and limited scalability. Platform-based models change that equation by consolidating data, intelligence, and governance within one integrated ecosystem. Cloud platforms such as Microsoft Azure, AWS, and Google Cloud provide banks with the scale, resilience, and compliance structures required to operationalize AI securely across all business units.

This shift is as much cultural as it is technical. Forward looking banks are redefining how decisions are made, embedding AI not as an experiment but as an operational layer. The difference lies in how intelligence is distributed, from frontline customer service to core treasury functions, allowing every process to learn continuously from data. When AI becomes part of the enterprise nervous system, efficiency and innovation naturally accelerate. Studies indicate that banks integrating AI across their value chain have reduced time to market for new financial products by nearly a third, while significantly improving predictive accuracy in risk assessment. The institutions leading this transformation are those that treat data and AI as shared infrastructure rather than departmental tools. The platform approach ensures transparency, governance, and agility, qualities that regulators, investors, and customers all demand. As markets become increasingly algorithmic, the banks that adapt their operating model now will not only stay compliant and cost-efficient but also position themselves as intelligent, learning enterprises ready for the decade ahead.

To understand how traditional banking architecture is evolving, it helps to visualize how different data systems, business functions, and customer channels are being unified under a single intelligent platform. The illustration below shows how a bank’s complex ecosystem, from branches to mobile apps, connects through an integrated enterprise backbone that supports analytics, governance, and decision intelligence.

This architecture represents the shift from siloed legacy systems to a connected, data-driven model. Each component, customer channels, enterprise services, data management, and analytics, feeds into a central integration layer that enables AI and machine learning to operate across the value chain. It highlights how financial institutions are modernizing their back-end frameworks to build a foundation where AI can deliver continuous insight and agility across all customer touchpoints and regulatory functions. By consolidating utility systems and information services under a unified governance framework, banks can ensure consistency, resilience, and faster innovation cycles aligned with compliance standards.

The Role of Microsoft Azure as the Enabler of Banking AI

How Azure’s unified data, AI, and governance stack is redefining scalability, security, and speed for modern banks.

Among the various enterprise ecosystems available, Microsoft Azure stands out for its depth, interoperability, and commitment to regulated industries like banking. Azure’s architecture allows financial institutions to unify their data sources, modernize legacy systems, and deploy AI models across geographies while maintaining compliance with stringent data residency and audit requirements. What differentiates Azure in this space is its ability to integrate core banking data, analytics pipelines, and generative AI capabilities in a single secured environment, a prerequisite for any institution looking to move from AI pilots to full-scale deployment. At its foundation, services such as Azure Data Lake, Synapse Analytics, and Microsoft Fabric enable a consistent data fabric across business functions. This consistency is vital for developing trustworthy AI models that can interpret customer behavior, transaction trends, and risk indicators in real time. Layered above this, Azure Machine Learning and Azure OpenAI Service offer banks tools to train, evaluate, and deploy models that power everything from fraud detection to personalized credit scoring. When these capabilities are governed by Azure Purview and secured through Azure Sentinel, the result is a transparent, traceable, and compliant AI ecosystem.

Beyond the infrastructure, Azure’s greatest advantage lies in how it blends enterprise-grade control with human-centric usability. Its integration with productivity tools such as Microsoft 365 and Copilot enables AI to flow naturally into the everyday workflows of relationship managers, analysts, and compliance officers. A loan manager can summarize hundreds of application documents in seconds, while a compliance team can automate anomaly reviews with traceable logic. This fusion of operational AI and workforce productivity transforms efficiency from a technical outcome into a cultural habit. Microsoft’s partnerships with major global banks have demonstrated this potential in practice. Through collaborations with Standard Chartered and Deutsche Bank, Azure has helped financial institutions establish secure AI innovation labs, migrate core operations to the cloud, and deploy autonomous systems that enhance resilience and customer trust. These examples reflect a wider trend where technology becomes an enabler of responsibility as much as performance, and where AI in banking is not only about speed or automation but about building reliable intelligence at scale.

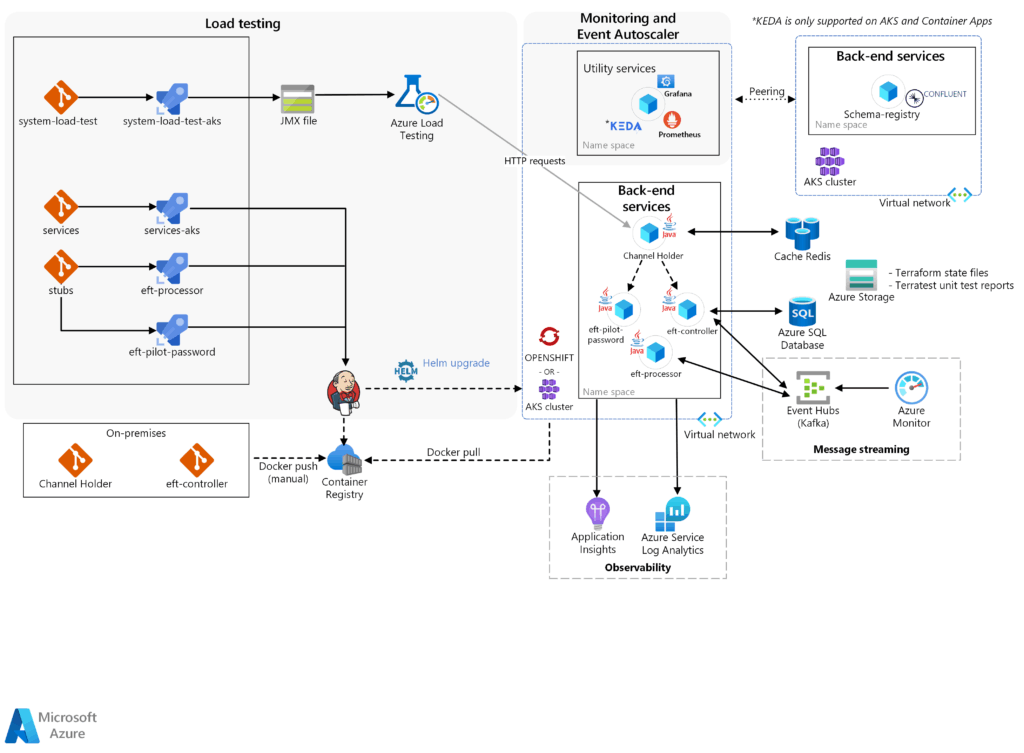

In modern banking, AI cannot operate effectively without a robust cloud infrastructure. Microsoft Azure provides that backbone — integrating data lakes, AI services, and compliance layers into one orchestrated ecosystem. The diagram below illustrates how an Azure-based architecture enables continuous testing, scaling, and monitoring of banking workloads in a secure, automated environment.

This visual demonstrates how Azure combines load testing, back-end services, monitoring tools, and observability frameworks to maintain reliable AI operations at scale. The orchestration between Azure Load Testing, Application Insights, SQL databases, and event hubs ensures that every component of the system remains optimized and traceable. For financial institutions, this design means that critical processes, such as fraud detection, real-time analytics, or model retraining, can run efficiently with automated scaling and security enforcement. It reflects the core strength of Azure’s ecosystem: bringing together DevOps, AI, and compliance workflows under one governed cloud platform.

What Good Enterprise-Banking AI Looks Like

Inside the anatomy of an intelligent bank, integrating models, data, and decisions into one continuous system.

A bank that has mastered AI is one that views its data and intelligence layers as live business assets rather than passive reporting systems. Instead of waiting for monthly dashboards or quarterly reviews, it embeds analytics and ML models into daily workflows so that every customer interaction, credit decision, and back-office event becomes an opportunity to learn and respond. That means personalising experiences in real time, optimising risk decisions quickly, and deploying intelligent automation not just to support human work, but to accelerate it. In practice, such banks often deploy AI across multiple functions, front, middle, and back office, and scale what works. For example, fraud detection might evolve into a self-learning engine that adapts to new patterns, while wealth-management services might shift from static product lists to personalised investment nudges in seconds. Research highlights that banks moving beyond pilots into enterprise-wide AI adoption tend to unlock productivity gains of 40 % or more and see measurable revenue uplift (Mckinsey)

The hallmark of this level of maturity is operationalisation: models aren’t deployed once and forgotten, but continuously monitored, updated, and integrated into business KPIs. These institutions also invest in capabilities: data engineers, ML ops, governance functions, and change management. A recent IBM discussion noted that AI is now “an imperative” rather than optional for banks that want to lead, emphasising the need for platform-based intelligence across all business lines. (IBM)

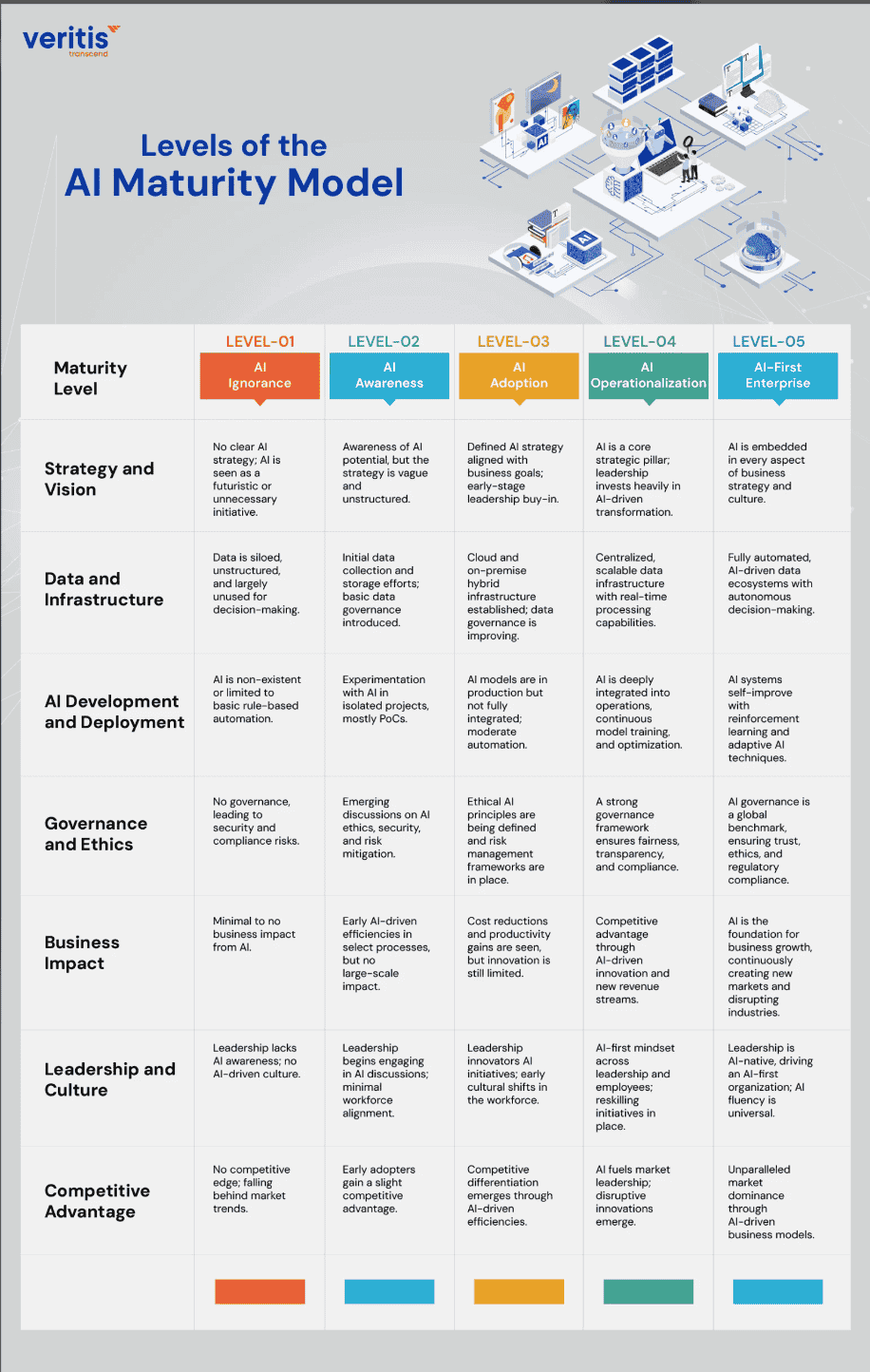

From our perspective, the banks that will thrive aren’t necessarily the first to experiment, but those that embed AI systems deeply into their infrastructure, culture and operations, enabling real-time decisions, continuous learning, and broad agility. In other words, good enterprise-banking AI is less about novelty and more about repeatable execution and business integration. To visualize what “good” looks like in AI-driven banking, it helps to examine how organizations evolve from isolated proofs-of-concept into fully intelligent enterprises. The diagram below outlines this maturity journey, showing how strategy, data, governance, and business impact expand across five stages of evolution.

The model illustrates that true maturity is not about having advanced algorithms, but about integrating intelligence into every business dimension. At Level 1 and 2, banks experiment with automation and analytics but lack governance or measurable outcomes. By Level 4 and 5, AI becomes embedded in daily operations, supported by robust ethics, strong data governance, and measurable cultural adoption. For banking leaders, reaching the upper tiers means transforming AI from a technical asset into an institutional capability that drives competitive advantage and customer trust.

Governance and Risk in AI-Driven Banking

As banks scale AI, governance and risk become front and centre. AI brings new dimensions of complexity, models may operate on opaque logic, the data underpinning them may bias outputs, and third-party dependencies (cloud, model vendors) introduce further vulnerabilities. Regulators and industry bodies have stressed that banks must adapt their existing risk-management frameworks to address these specific AI concerns. (BPI)

Governance in this context means clear roles, documented policies, traceability of data and model decisions, rigorous monitoring for drift, and a framework for human-in-the-loop oversight. For example, a bank may use generative AI to draft credit summaries, but ensure every summary is audited, logged and subject to rollback if the model’s behaviour strays, this is not optional, it’s essential for trust and compliance. According to an industry report, banks failure to adopt such practices risk not only regulatory sanctions but also reputational damage and loss of customer confidence. Risk management for AI also spans third-party and systemic considerations. One risk is model concentration, if a large number of banks rely on the same model provider or cloud infrastructure, a single failure could cascade. Banks need to build resilience into their supply-chain, test for adversarial attacks, and maintain fallback processes. From our vantage point, this means investing in model assurance platforms, continuous audit logs and scenario-based stress testing that includes AI-specific threats. Finally, the governance narrative is not just about compliance; it supports the business.

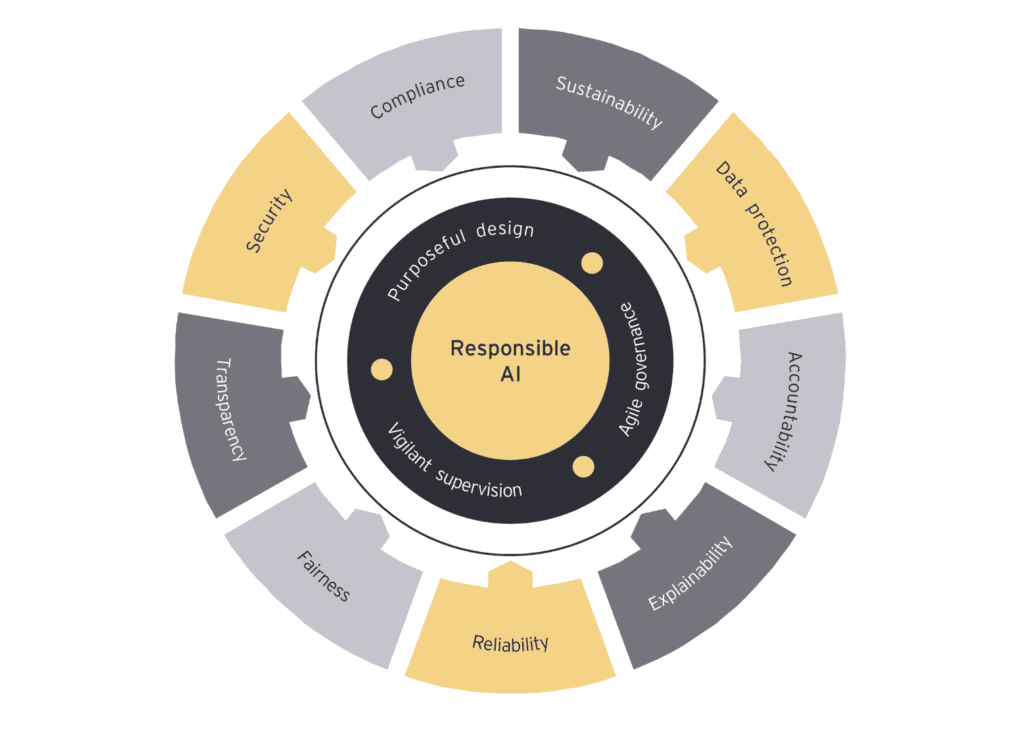

When banks combine strong governance with agile deployment, they build trust with customers and regulators alike, a competitive differentiator in an environment where data ethics and algorithmic transparency are increasingly visible. In short, the smart bank treats risk not as an afterthought, but as a core enabler of scalability and value. Responsible AI is becoming the foundation of risk management for financial institutions. As banks integrate AI deeper into their operations, they must ensure that every model, dataset, and decision process aligns with ethical and regulatory expectations. A well-defined governance model brings structure to this responsibility, helping institutions balance innovation with control. The following framework captures the interconnected dimensions of a mature AI governance ecosystem.

This framework demonstrates how effective AI governance goes far beyond compliance checklists. It emphasizes principles such as transparency, fairness, accountability, and explainability, which are critical for maintaining stakeholder trust and regulatory confidence. The inner layers, purposeful design, agile governance, and vigilant supervision, illustrate the operational mechanisms that sustain responsible AI over time. When applied in banking, this model ensures that algorithms operate within defined ethical and legal boundaries while still enabling innovation and efficiency. It also highlights that responsible AI is not static; it requires continuous oversight, updates to meet new regulations, and cross-functional collaboration between data scientists, compliance leaders, and technology partners.

Stay Informed with Yallo Group!

Unlock the latest insights, news, and expert advice—straight to your inbox!

👉 Subscribe to our Newsletter

📝 Explore Our Latest Blogs

How to Adopt AI in Banking: Four Foundational Moves

The Evolution of Personalized Engagement

Adopting AI in banking is not a one-time project; it is a gradual re-architecture of how intelligence flows through the enterprise. Most financial institutions today find themselves somewhere between proof-of-concept and selective deployment. The journey toward scaled, responsible AI requires four foundational moves, rethinking data, technology, governance, and talent in a single motion. The banks that have made visible progress are those that treat these dimensions as parts of one operating model rather than as separate initiatives. The first move is data unification. Banks cannot build intelligent systems on fragmented data foundations. A unified data fabric that consolidates structured and unstructured information, transactions, risk profiles, communications, customer history, becomes the bedrock for reliable AI. Microsoft’s Fabric and Synapse Analytics solutions, for example, are enabling institutions to integrate data sources without duplicating them, ensuring models train on accurate, compliant information. This foundation is not just technical; it also establishes a shared vocabulary for how the business defines metrics, risk, and value.

The second move is modernizing the core technology stack. Migrating legacy workloads to flexible cloud architectures allows AI pipelines to run efficiently and at scale. Financial organizations that embrace Azure Machine Learning or Google Vertex AI have seen significant reductions in model deployment times, in some cases cutting integration cycles from months to weeks. This agility lets teams experiment faster and operationalize models directly within production environments, ensuring that AI becomes part of the decision-making process rather than a disconnected analytics layer. The third move centers on building robust governance and risk controls. Effective AI adoption requires the same discipline that banks apply to capital adequacy or cybersecurity. Human-in-the-loop review, explainability mechanisms, and audit trails must be embedded from the start. Institutions such as Standard Chartered have implemented internal “AI assurance frameworks” that combine regulatory oversight with data lineage tracking, ensuring accountability for every automated outcome. Such governance enables innovation without compromising compliance, giving regulators and customers confidence in AI-enabled services. Finally, banks must invest in new talent and operating models. AI success depends not only on algorithms but on the collaboration between data scientists, compliance leaders, and domain experts. Forward-looking banks are creating “fusion teams” that combine engineering, risk, and product functions to bridge the gap between technology and business intent.

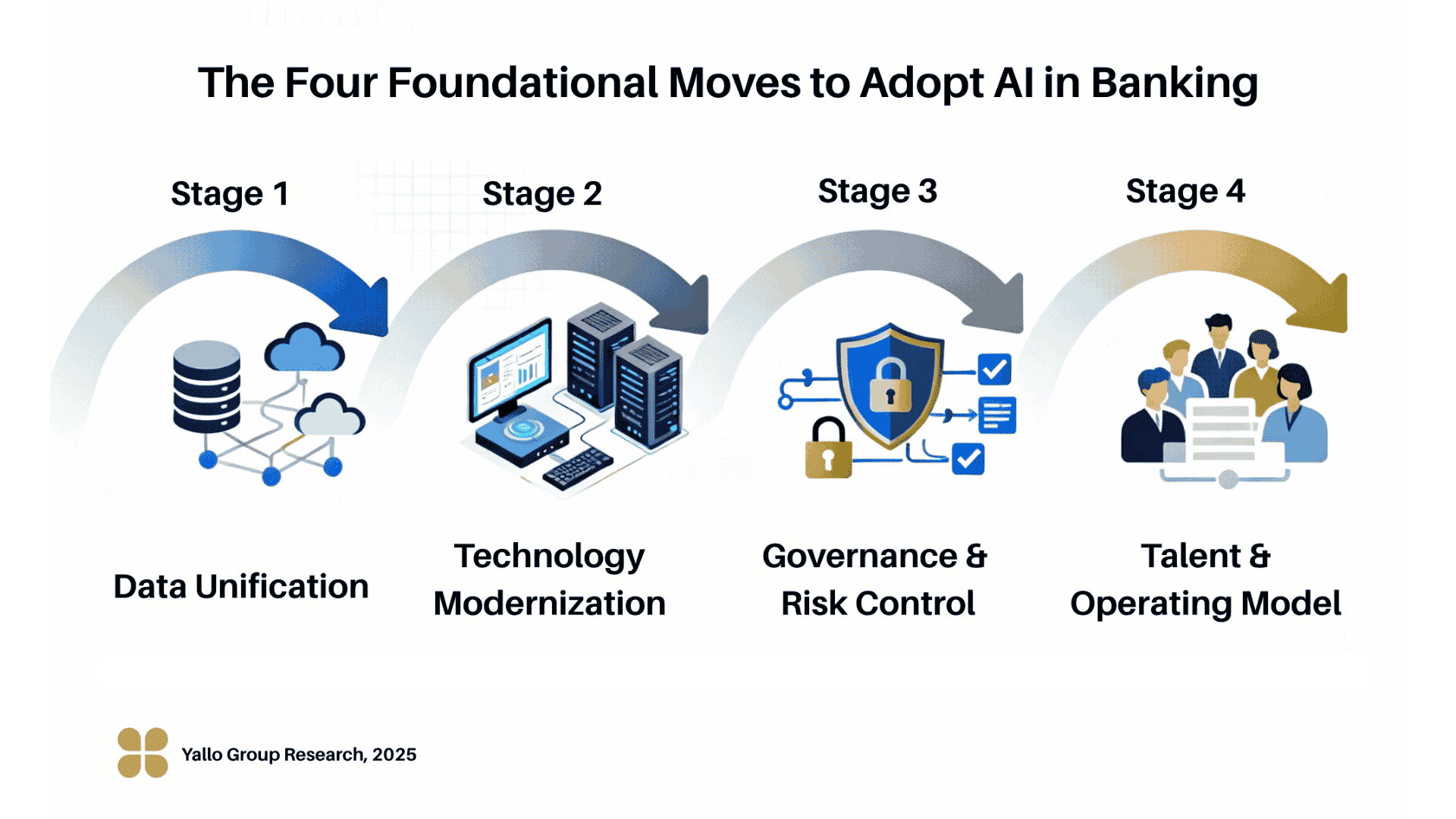

According to Accenture, banks adopting such interdisciplinary structures have achieved productivity gains of over 20 percent and report fewer compliance escalations, as model outputs are contextualized by domain expertise. Together, these four moves define a practical, repeatable roadmap for scaling AI in banking. They do not rely on massive reinvention but on connecting existing capabilities under a unified, governed, and data-centric architecture. This integrated approach transforms AI from an experimental technology into an enterprise advantage, one that continuously learns, adapts, and compounds value across every layer of the bank. To make the adoption journey tangible, it helps to view the transformation as a structured sequence rather than a series of experiments. The following roadmap visualizes the four foundational moves that define how banks can scale AI responsibly and effectively, from unifying their data to transforming their operating culture.

This roadmap encapsulates the phased evolution of AI adoption in financial institutions. It begins with data unification, where banks consolidate fragmented datasets and establish a single source of truth. From there, technology modernization introduces the scalable cloud and machine-learning infrastructure required for reliable deployment. The third stage, governance and risk control, reinforces compliance, model security, and ethical standards, ensuring AI operates transparently within regulatory frameworks. Finally, talent and operating model transformation embeds AI into daily workflows through multidisciplinary collaboration between technology, risk, and business teams. Together, these four stages represent not just a technical implementation, but an organizational rewiring toward intelligence, agility, and trust.

Measuring Success, From Proof to Performance

Predict, Produce, and Personalize at Scale

As AI moves from prototypes to production, success can no longer be measured by technical completion alone. Banks that have matured their AI programs are defining success in terms of business outcomes, trust, and adaptability rather than only precision metrics. The most effective institutions treat AI performance management as part of enterprise performance management, blending technological indicators with human and financial dimensions. Traditional metrics like model accuracy and recall are still relevant, but they now sit alongside broader key performance indicators such as decision latency, automation coverage, customer satisfaction, and model rollback rates. Leading banks, for instance, are tracking the percentage of AI-generated insights that lead to actionable decisions within a specific timeframe — a direct measure of AI’s impact on agility and responsiveness. In parallel, the inclusion of explainability scores ensures that models are not just efficient but also interpretable to auditors and regulators.

Beyond metrics, trust is emerging as a measurable outcome. The effectiveness of an AI system in banking depends not only on its accuracy but on the institution’s ability to demonstrate fairness, transparency, and accountability. A 2025 report by the World Economic Forum emphasizes that financial organizations adopting transparent AI governance practices experience significantly higher customer trust scores and lower attrition rates than those relying on opaque automation. Trust, therefore, becomes both a moral and commercial currency. The next frontier in measurement is adaptability, how fast a bank’s AI system can learn and improve over time. This involves tracking the half-life of models, the frequency of retraining cycles, and the speed at which insights move from lab environments to customer-facing processes. The most advanced institutions are already building internal “AI observability dashboards” that track these indicators across hundreds of models in production, giving leadership real-time visibility into systemic performance. Ultimately, measuring AI success in banking is about linking intelligence to outcomes that matter: stronger compliance, faster risk detection, deeper customer engagement, and sustained profitability. When metrics evolve from isolated scores to enterprise impact, AI ceases to be a cost center and becomes a driver of strategic differentiation.

Where This Is Going, The Next Frontier of AI in Banking

The next stage of AI in banking will be defined by the shift from intelligence to autonomy. Until now, banks have focused on building predictive systems that assist human decision making. The next frontier is agentic AI, systems that can plan, act, and self-correct within controlled boundaries. In this model, AI becomes an operational participant rather than a passive recommender. A trading assistant might autonomously rebalance portfolios under defined risk thresholds, or a compliance agent could continuously test transactions against evolving regulations and generate alerts without human prompts. These capabilities are already being piloted in several global institutions as part of their move toward “autonomous finance.” This evolution is supported by advances in enterprise agent frameworks, which combine planning models, memory components, and tool-use capabilities governed by policy layers. Microsoft, for instance, has been integrating these frameworks into Azure’s enterprise AI stack, allowing regulated organizations to test controlled autonomy with traceable logic and rollback features. The upcoming Azure AI Studio updates focus on embedding governance natively into agent orchestration, giving banks the ability to experiment with autonomy while maintaining full compliance.

As these systems mature, the role of humans will evolve from supervision to strategic orchestration. Instead of monitoring every action, teams will design frameworks for decision limits, escalation rules, and ethical boundaries. The combination of machine autonomy and human intent will create hybrid decision ecosystems where agents perform high-frequency reasoning tasks while humans focus on judgment, relationships, and innovation. Early pilots in North America and Europe have already demonstrated measurable efficiency gains, with process automation reaching up to 60 percent of manual workloads in certain treasury operations. However, the transition toward agentic AI will require a careful balance of innovation and responsibility. Banks will need to prove that autonomous systems can operate reliably within regulatory frameworks such as the EU AI Act and local financial supervisory requirements. This will drive demand for explainable-agent platforms, continuous monitoring, and new forms of operational certification. In essence, the future of banking AI will be less about the technology itself and more about how institutions govern digital autonomy, designing systems that are both powerful and accountable.

Building the Intelligent Bank of the Future

Artificial intelligence is no longer an experiment sitting at the edges of the banking organization; it is becoming its core operating logic. The institutions that will lead the next decade are those that view AI not as a project but as an enterprise capability, one that shapes every business decision, customer interaction, and compliance workflow. AI is transforming banking from a system of transactions into a system of intelligence. The foundation of that shift lies in how effectively banks can unite technology, governance, and culture under a single purpose: to deliver smarter, safer, and more personalized financial value. To achieve this, leadership commitment will matter as much as infrastructure. The journey toward an AI driven enterprise is as cultural as it is technical. Executive teams must champion responsible AI frameworks, foster collaboration between data and business units, and ensure that innovation aligns with long-term trust. Those who invest early in AI talent, governance maturity, and interoperable platforms like Microsoft Azure will not only capture efficiency but also build resilience in an increasingly unpredictable market.

Looking ahead, the banks that succeed will be those that learn faster than change itself. They will continuously refine their models, adapt governance to new regulations, and experiment boldly with human machine collaboration. AI will not replace banking professionals; it will amplify them, giving every decision maker access to context, foresight, and precision at a scale once unimaginable. This is the essence of intelligent banking: a future where every process, product, and relationship benefits from the fusion of human insight and machine intelligence. In a decade defined by digital autonomy and customer trust, the intelligent bank will be one that thinks before it acts, learns before it speaks, and builds technology not just for speed but for stewardship. The foundations are already visible today, what remains is leadership bold enough to turn potential into permanence.

Learn More Through Yallo Group

Explore more insights on global technology strategy, AI governance, and innovation through Yallo Group’s Case Studies and Insights, where we decode how emerging technologies reshape economies and drive sustainable growth.